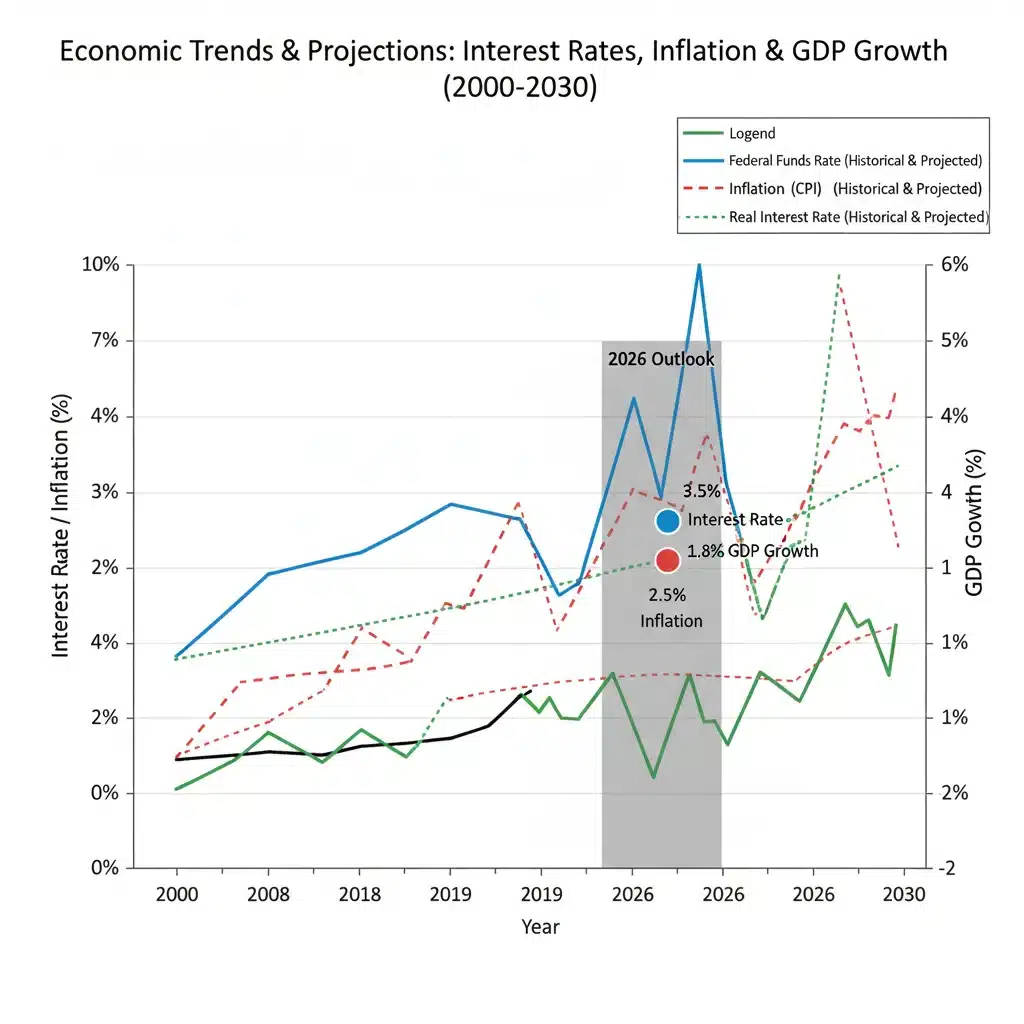

Federal Reserve 2026: Interest Rate Hikes and Investor Outlook

Anúncios

Navigating the 2026 Federal Reserve Interest Rate Hikes: A 3-Month Outlook for U.S. Investors

The financial landscape is ever-evolving, and few entities wield as much influence over its direction as the Federal Reserve. As we cast our gaze towards 2026, the prospect of further Federal Reserve 2026 interest rate hikes looms large, presenting both challenges and opportunities for U.S. investors. Understanding the potential trajectory of these rates, the underlying economic factors driving them, and the strategic adjustments necessary to navigate this environment is paramount. This comprehensive guide will delve into a 3-month outlook, dissecting key indicators, potential impacts across various asset classes, and offering actionable insights to help you optimize your investment portfolio.

Anúncios

The Federal Reserve’s primary mandate is to foster maximum employment and price stability. In recent years, the battle against persistent inflation has been a central theme, leading to a series of aggressive rate increases. While 2026 might seem a distant horizon, the market often prices in future expectations well in advance. Therefore, proactive analysis of the Fed’s likely actions and their ramifications is not just prudent, but essential for safeguarding and growing your wealth.

Anúncios

Understanding the Federal Reserve’s Mandate and Tools

Before we project into the future, it’s crucial to grasp the fundamental role of the Federal Reserve and the mechanisms it employs to achieve its objectives. The Fed’s dual mandate – maximum employment and price stability – often requires a delicate balancing act. When inflation runs hot, the Fed typically raises the federal funds rate, making borrowing more expensive and thereby cooling down economic activity. Conversely, during periods of economic slowdown or recession, it lowers rates to stimulate growth.

The federal funds rate is the target interest rate set by the Federal Open Market Committee (FOMC) for overnight borrowing between banks. While it’s an overnight rate, its changes ripple through the entire financial system, influencing everything from mortgage rates and credit card interest to corporate borrowing costs and bond yields. Therefore, any discussion about Federal Reserve 2026 actions inevitably centers on this pivotal rate.

Key Tools of the Federal Reserve:

- Federal Funds Rate: As mentioned, this is the primary tool for influencing short-term interest rates.

- Quantitative Easing (QE) and Quantitative Tightening (QT): These involve the Fed buying or selling government securities and other assets to inject or withdraw liquidity from the financial system, impacting long-term interest rates.

- Reserve Requirements: The amount of funds banks must hold in reserve. Changes here can impact the amount of money banks have available to lend.

- Discount Rate: The interest rate at which commercial banks can borrow directly from the Federal Reserve.

The decisions made by the FOMC are not taken lightly. They are the result of extensive analysis of a vast array of economic data, including inflation reports, employment figures, GDP growth, consumer spending, and global economic conditions. Predicting the Federal Reserve 2026 moves requires a deep dive into these same indicators and an understanding of the Fed’s forward guidance.

Economic Landscape Leading to 2026: What Drives the Fed’s Decisions?

Several key economic factors will undoubtedly shape the Federal Reserve’s decisions regarding interest rates in 2026. Understanding these drivers is crucial for anticipating their actions.

Inflationary Pressures:

Inflation remains a significant concern. While supply chain disruptions may have eased, other factors like wage growth, geopolitical events, and fiscal policy can continue to exert upward pressure on prices. The Fed’s target inflation rate is typically around 2%. If inflation remains stubbornly above this target as we approach and enter 2026, the likelihood of continued rate hikes increases significantly. Conversely, if inflation moderates consistently towards the target, the Fed might adopt a more dovish stance, potentially pausing or even cutting rates.

Labor Market Strength:

A robust labor market, characterized by low unemployment rates and strong wage growth, often provides the Fed with room to raise rates without fear of triggering a significant economic downturn. However, an excessively tight labor market can also contribute to inflationary pressures. The Fed will be closely monitoring metrics like the unemployment rate, job openings, and average hourly earnings for signs of overheating or cooling in the job market.

GDP Growth and Economic Activity:

The overall health of the U.S. economy, as measured by Gross Domestic Product (GDP) growth, is another critical determinant. A strong economy can generally absorb higher interest rates, while a slowing economy might necessitate a more cautious approach from the Fed. Consumer spending, business investment, and manufacturing output will all be under the microscope.

Global Economic Conditions:

The U.S. economy does not exist in a vacuum. Global economic slowdowns, geopolitical instability, and currency fluctuations can all influence the Federal Reserve’s decisions. For instance, a stronger U.S. dollar, often a byproduct of higher U.S. interest rates, can make U.S. exports more expensive and imports cheaper, impacting domestic businesses and inflation.

Analyzing these interconnected factors provides a framework for understanding the potential scenarios for Federal Reserve 2026 interest rate policy. It’s a complex puzzle, and the pieces are constantly shifting.

3-Month Outlook for U.S. Investors Ahead of Federal Reserve 2026 Hikes

Let’s project a 3-month outlook for U.S. investors, considering the potential for Federal Reserve 2026 interest rate adjustments. This period will be crucial for positioning portfolios effectively.

Month 1: Initial Market Reactions and Data Scrutiny

In the initial month of our outlook, markets will likely be highly sensitive to any new economic data releases and comments from Fed officials. Inflation reports (CPI, PCE), employment figures (non-farm payrolls, unemployment rate), and consumer confidence surveys will be scrutinized for any signs that might alter the Fed’s path. Investors should anticipate:

- Increased Volatility: Equity and bond markets may experience heightened volatility as investors react to incoming data and adjust their expectations for future rate hikes.

- Flight to Quality: In periods of uncertainty, some investors may move towards safer assets like U.S. Treasury bonds, potentially causing their yields to fluctuate.

- Sector Rotation: Growth stocks, which are often more sensitive to interest rate changes due to their reliance on future earnings, might face headwinds. Value stocks, particularly those with strong cash flows and less reliance on debt, could perform relatively better.

During this period, active monitoring of economic calendars and Fed speeches will be paramount. Investors should revisit their risk tolerance and ensure their portfolio allocation aligns with their long-term goals.

Month 2: Confirmation or Contradiction of Trends

By the second month, we should start to see clearer trends emerging from the economic data. If inflation continues to cool and the labor market shows signs of moderating without a significant increase in unemployment, the market might begin to price in a more measured approach from the Fed. Conversely, persistent inflation or an unexpectedly strong economy could reinforce expectations of continued aggressive hikes.

Potential developments include:

- Bond Market Adjustments: If the outlook for Federal Reserve 2026 hikes becomes clearer, bond yields will adjust accordingly. Shorter-term yields are more directly influenced by Fed policy, while longer-term yields also incorporate inflation expectations and economic growth prospects.

- Corporate Earnings Focus: Investors will pay close attention to corporate earnings reports. Companies with strong pricing power and efficient operations will be better positioned to weather higher interest rates and potential economic slowdowns.

- Real Estate Market Nuances: Higher mortgage rates, a direct consequence of Fed hikes, can cool the housing market. Investors in real estate should assess regional market conditions and consider the impact on property values and rental yields.

This month will be about confirming initial hypotheses and making tactical adjustments based on the evolving data. Diversification remains a key strategy.

Month 3: Preparing for the 2026 Horizon

As we approach the end of our 3-month outlook, the market will increasingly focus on the consensus view regarding Federal Reserve 2026 actions. By this point, analysts will have a more refined understanding of the Fed’s likely stance, and investors can make more informed strategic decisions.

Key considerations for investors:

- Re-evaluating Fixed Income: With a clearer picture of future rates, investors can re-evaluate their fixed-income portfolios. Shorter-duration bonds might be preferred in a rising rate environment, as they are less sensitive to interest rate changes than long-duration bonds. Consider laddering bond maturities to mitigate interest rate risk.

- Equity Sector Analysis: Certain sectors tend to perform better during periods of rising rates. Financials, which often benefit from higher net interest margins, and energy, due to its inflation-hedging properties, could be areas of focus. Conversely, highly leveraged companies or those in discretionary consumer sectors might face greater challenges.

- Alternative Investments: Explore alternative investments that may offer diversification and potential inflation protection, such as commodities or certain types of real estate.

- Dollar Strength and International Exposure: Higher U.S. interest rates can strengthen the dollar. This can impact the returns on international investments for U.S. investors, as foreign currency earnings translate into fewer dollars. Consider hedging currency risk if significant international exposure is maintained.

This final month of the outlook is about solidifying your investment strategy for the challenges and opportunities that 2026 may bring, armed with the latest economic intelligence.

Impact on Various Asset Classes for U.S. Investors

The Federal Reserve’s actions in 2026 will not affect all asset classes equally. Here’s a breakdown of potential impacts:

Equities:

- Growth vs. Value: As mentioned, growth stocks, particularly those with high price-to-earnings ratios, can be vulnerable to rising rates because their future earnings are discounted at a higher rate. Value stocks, often mature companies with stable cash flows, may be more resilient.

- Sector Performance: Financials often benefit from higher rates. Utilities and real estate investment trusts (REITs), which are often seen as bond proxies due to their dividend payouts, can be negatively impacted as their yields become less attractive compared to rising bond yields.

- Corporate Debt: Companies with significant floating-rate debt will see their interest expenses rise, potentially impacting profitability.

Fixed Income (Bonds):

- Inverse Relationship with Yields: Bond prices generally move inversely to interest rates. When the Fed raises rates, existing bonds with lower coupon rates become less attractive, causing their prices to fall.

- Duration Risk: Longer-duration bonds are more sensitive to interest rate changes. In a rising rate environment, investors might prefer shorter-duration bonds or bond funds.

- Treasuries vs. Corporate Bonds: U.S. Treasury yields serve as a benchmark. Corporate bond yields will also rise, with credit spreads reflecting the perceived risk of corporate defaults.

Real Estate:

- Mortgage Rates: Higher federal funds rates translate into higher mortgage rates, increasing the cost of homeownership and potentially slowing down the housing market.

- Commercial Real Estate: Financing costs for commercial properties will also rise, which can impact property valuations and development projects. Rental income and vacancy rates will be key metrics to watch.

Commodities:

- Inflation Hedge: Some commodities, like gold and oil, are often viewed as inflation hedges. If inflation remains a concern into 2026, these assets might see increased demand.

- Dollar Strength: A stronger U.S. dollar can make dollar-denominated commodities more expensive for international buyers, potentially dampening demand.

Currencies:

- Stronger Dollar: Higher U.S. interest rates typically attract foreign capital, leading to a stronger U.S. dollar relative to other currencies. This can make U.S. goods more expensive for foreign buyers and foreign goods cheaper for U.S. consumers.

Understanding these nuanced impacts is critical for U.S. investors to adjust their portfolios strategically in anticipation of Federal Reserve 2026 actions.

Strategic Adjustments for U.S. Investors

Given the potential for Federal Reserve 2026 interest rate hikes, U.S. investors should consider the following strategic adjustments:

1. Reassess Your Portfolio Allocation:

Review your current asset allocation to ensure it aligns with your risk tolerance and long-term financial goals in a rising rate environment. Consider whether your exposure to interest-rate-sensitive assets is appropriate.

2. Focus on Quality and Strong Fundamentals:

In equities, prioritize companies with strong balance sheets, robust cash flows, manageable debt levels, and proven profitability. These companies are generally better equipped to withstand higher borrowing costs and economic uncertainties.

3. Shorten Fixed Income Duration:

If you hold bonds, consider shortening the duration of your fixed-income portfolio. This can be achieved by investing in shorter-term bonds or bond funds, which are less susceptible to price declines when interest rates rise. Explore floating-rate notes, which adjust their coupon payments with prevailing interest rates.

4. Explore Dividend-Paying Stocks with Growth Potential:

While some high-yield dividend stocks (like REITs and utilities) can struggle in a rising rate environment, companies that consistently grow their dividends and have strong underlying businesses can provide both income and capital appreciation. Focus on companies with sustainable dividend growth rather than just high current yields.

5. Diversify Geographically and Across Asset Classes:

Don’t put all your eggs in one basket. Diversifying across different countries and a variety of asset classes (equities, bonds, real estate, commodities, alternatives) can help mitigate risks and capture opportunities wherever they arise. A stronger dollar might make international investments less attractive initially, but opportunities can still exist.

6. Consider Inflation-Protected Securities (TIPS):

Treasury Inflation-Protected Securities (TIPS) are government bonds designed to protect investors from inflation. Their principal value adjusts with the Consumer Price Index (CPI), providing a hedge against rising prices, which is a key driver for Federal Reserve 2026 policy.

7. Review Your Debt Obligations:

If you have variable-rate debt (e.g., certain mortgages, lines of credit), rising interest rates will increase your payments. Consider locking in fixed rates where possible or developing a plan to pay down high-interest debt more aggressively.

8. Stay Informed and Adaptable:

The economic landscape is dynamic. Continuously monitor economic data, Federal Reserve communications, and geopolitical developments. Be prepared to adapt your investment strategy as new information becomes available. Flexibility is a key attribute of successful investors.

Potential Scenarios for Federal Reserve 2026

While predicting the future with absolute certainty is impossible, we can outline a few potential scenarios for the Federal Reserve 2026 and their implications:

Scenario 1: Continued Gradual Hikes

In this scenario, inflation remains somewhat elevated but manageable, and the economy continues to grow at a moderate pace. The Fed opts for a series of smaller, gradual rate hikes throughout 2026 to ensure inflation returns to its target without stifling economic growth. This would likely lead to a continued but slower rise in bond yields and a more cautious equity market, favoring value and defensive sectors.

Scenario 2: Aggressive Hikes Due to Persistent Inflation

If inflation proves more stubborn than anticipated, perhaps due to renewed supply shocks or strong wage growth, the Fed might be forced to implement more aggressive rate hikes. This could lead to a more significant slowdown in economic activity, potentially even a mild recession. In this environment, equities would likely face stronger headwinds, and bond yields could spike. Defensive strategies and capital preservation would be paramount.

Scenario 3: Pause or Rate Cuts Due to Economic Slowdown

Conversely, if the economy slows down significantly, perhaps entering a recession, and inflation moderates rapidly, the Fed might pause its rate hikes or even begin to cut rates to stimulate growth. This would likely be positive for growth stocks and could lead to a rally in both equity and bond markets as investors anticipate easier monetary policy.

Each scenario presents a unique set of challenges and opportunities. The key for investors is to build a resilient portfolio that can navigate different economic climates rather than trying to perfectly time the market.

The Importance of Long-Term Perspective

Amidst the short-term volatility and speculation surrounding Federal Reserve 2026 actions, it’s crucial for U.S. investors to maintain a long-term perspective. Market cycles are a natural part of investing, and periods of rising interest rates, while challenging, are not uncommon. Historically, disciplined investors who stick to a well-thought-out plan, diversify effectively, and regularly rebalance their portfolios tend to achieve their financial objectives.

Avoid making rash decisions based on headlines or short-term market fluctuations. Consult with a qualified financial advisor to develop a personalized investment strategy that considers your individual financial situation, risk tolerance, and long-term goals. They can help you understand how potential Federal Reserve 2026 policies might impact your specific portfolio and guide you in making informed adjustments.

Conclusion: Preparing for the Future of Federal Reserve 2026

The path of the Federal Reserve 2026 interest rates will be a defining factor for U.S. investors in the coming years. While the exact timing and magnitude of any hikes remain uncertain, a proactive and informed approach is essential. By understanding the Fed’s mandate, analyzing key economic indicators, and considering the potential impacts across various asset classes, investors can position themselves strategically.

The 3-month outlook suggests a period of intense data scrutiny and potential market volatility, transitioning into a phase where clearer trends emerge and strategic adjustments become more defined. Focusing on quality assets, managing duration risk in fixed income, diversifying broadly, and maintaining a long-term perspective will be critical elements of a successful investment strategy. The future is uncertain, but with careful planning and continuous learning, U.S. investors can confidently navigate the evolving economic landscape and strive towards their financial aspirations.