Fed Rate Hike: Impact on Consumer Lending Explained

Anúncios

The financial world recently buzzed with a significant announcement: the Federal Reserve adjusted its benchmark interest rate by a notable 0.50%. This move, while seemingly a technicality for some, carries profound implications that will ripple through the economy, directly impacting the average consumer, especially in the realm of lending. Understanding the nuances of this Fed rate hike is not just for economists; it’s crucial for anyone with a mortgage, a credit card, or plans for a future loan. Over the next six months, we can expect to see tangible shifts in how consumer lending operates, and being prepared is key to navigating these changes successfully.

For many, the Federal Reserve’s actions might feel abstract, a distant force influencing the economy. However, its decisions are deeply intertwined with our daily financial lives. The federal funds rate, which the Fed directly influences, serves as the foundation for a myriad of other interest rates across the financial system. When this rate moves, so do the costs associated with borrowing money for everything from buying a home to financing a car, or even just carrying a balance on a credit card. This particular Fed rate hike of 0.50% is a significant step, indicating the Fed’s commitment to addressing specific economic conditions, primarily inflation.

Anúncios

In this comprehensive guide, we will delve into what this latest Fed rate hike truly means for consumer lending. We’ll break down the immediate and projected impacts on various loan types, including mortgages, credit cards, and personal loans. Furthermore, we’ll explore the broader economic context driving these changes and, most importantly, provide actionable strategies and expert advice to help you adapt your financial planning and decision-making over the coming half-year. Whether you’re a prospective homebuyer, someone managing existing debt, or simply looking to understand the economic landscape better, this article will equip you with the knowledge needed to thrive in a changing financial environment.

Anúncios

Understanding the Federal Reserve’s Decision: Why a 0.50% Fed Rate Hike Now?

To grasp the implications of the recent Fed rate hike, it’s essential to first understand the Federal Reserve’s role and the motivations behind its monetary policy decisions. The Fed, as the central bank of the United States, has a dual mandate: to maximize employment and maintain price stability (i.e., control inflation). When inflation rises beyond its target, as it has been in recent times, the Fed often resorts to increasing interest rates as a tool to cool down the economy.

The Mechanics of a Rate Hike

The Federal Reserve doesn’t directly set the interest rates consumers pay. Instead, it influences the federal funds rate, which is the target rate for overnight lending between banks. When the Fed raises this target, it makes it more expensive for banks to borrow from each other. These increased borrowing costs are then passed on to consumers and businesses in the form of higher interest rates on various loans and credit products. A 0.50% increase, often referred to as a ‘half-point’ hike, is a more aggressive move than the typical 0.25% adjustments, signaling a stronger stance against inflation.

Economic Context: Inflation and Economic Growth

The primary driver for this particular Fed rate hike is the persistent inflationary pressure observed across the economy. Factors such as supply chain disruptions, strong consumer demand, and geopolitical events have contributed to rising prices for goods and services. By increasing interest rates, the Fed aims to reduce demand by making borrowing less attractive, thereby slowing down economic activity and, in theory, bringing inflation back down towards its long-term target. However, there’s always a delicate balance; too aggressive a hike could risk tipping the economy into a recession, while too little action might allow inflation to become entrenched.

The decision to implement a 0.50% Fed rate hike reflects the central bank’s assessment of the current economic climate and its forward-looking projections. It signals a commitment to reigning in inflation, even if it means some short-term pain in the form of higher borrowing costs. This move is part of a broader strategy that often involves a series of rate adjustments over time, depending on how economic indicators evolve. Consumers and businesses alike need to pay close attention to these signals, as they dictate the future cost of money.

Direct Impact on Consumer Lending: The Next 6 Months

The 0.50% Fed rate hike will not affect all types of consumer lending equally or immediately. However, over the next six months, nearly all forms of consumer credit will experience some degree of upward pressure on interest rates. Let’s break down the specific impacts on key lending products.

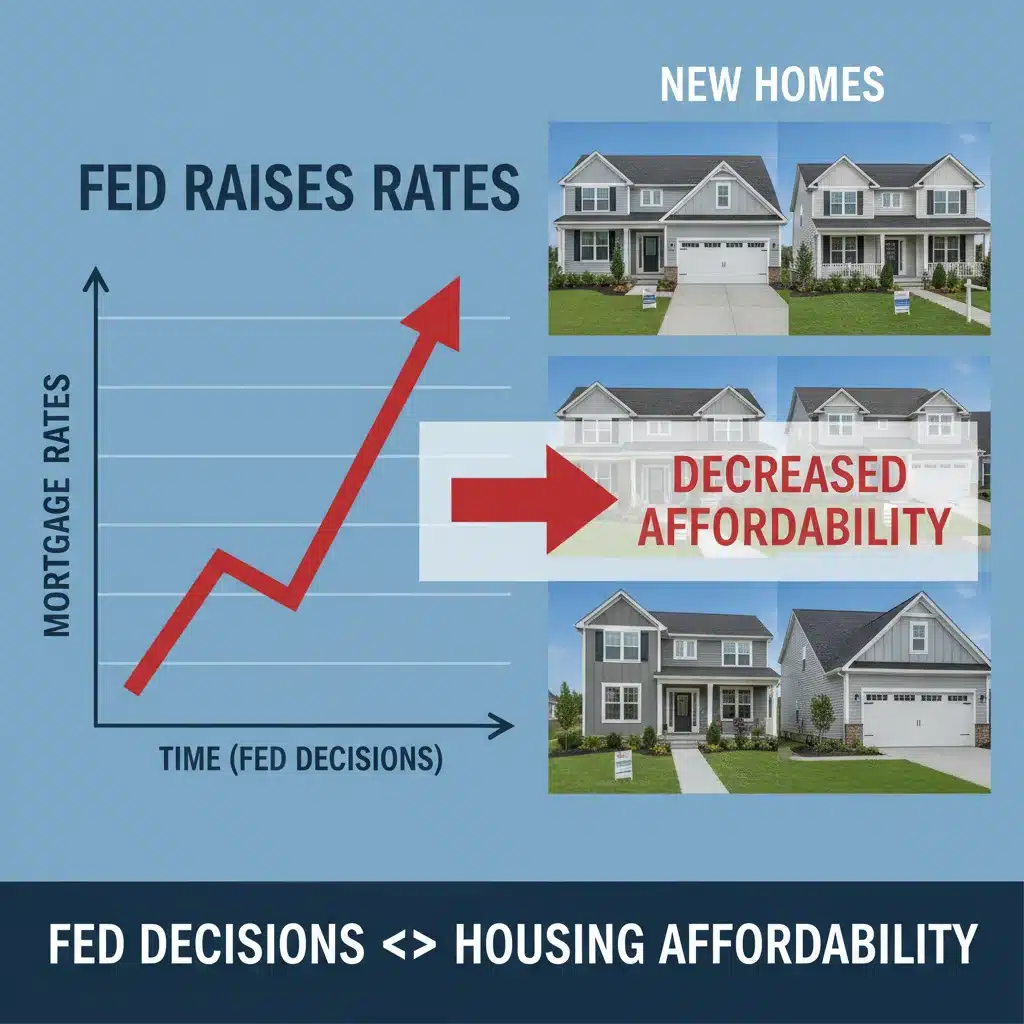

Mortgages: A Significant Shift

Mortgages are often the first area where consumers feel the effects of Fed rate changes. While the federal funds rate doesn’t directly set mortgage rates, it heavily influences them through the broader bond market, particularly the yield on 10-year Treasury bonds. Here’s what to expect:

- New Mortgages: Prospective homebuyers will likely face higher interest rates on both fixed-rate and adjustable-rate mortgages (ARMs). This means a higher monthly payment for the same loan amount, reducing purchasing power and making homeownership less affordable for some. The increased cost could also cool down the red-hot housing market in certain regions.

- Adjustable-Rate Mortgages (ARMs): For those with existing ARMs, the upcoming adjustment periods could lead to significant increases in their monthly payments. Homeowners with ARMs should review their loan terms and consider refinancing into a fixed-rate mortgage if rates are still favorable, or if they anticipate further rate hikes.

- Refinancing: The window for attractive refinancing opportunities may be closing or already closed for many. While some homeowners might still find value in refinancing to a lower rate, the overall trend will be towards higher rates, making refinancing less appealing unless it’s to shorten the loan term or tap into equity.

The housing market is particularly sensitive to interest rate fluctuations. A substantial Fed rate hike like this can lead to a slowdown in sales, a moderation in home price appreciation, and a shift in buyer sentiment. Over the next six months, we might see fewer bidding wars and a more balanced market, though this will vary by region.

Credit Cards: Immediate and Direct Impact

Credit card interest rates are often directly tied to the prime rate, which moves in lockstep with the federal funds rate. Therefore, the impact of a Fed rate hike on credit cards is usually swift and direct:

- Higher APRs: Consumers carrying a balance on their credit cards will almost immediately see their Annual Percentage Rates (APRs) increase. This translates to higher interest charges and larger minimum payments, making it more expensive to carry debt.

- New Card Offers: While introductory APRs might still be competitive, the standard variable APRs for new credit card offers will also likely climb.

- Strategies for Cardholders: This is a critical time for consumers with credit card debt to prioritize paying down high-interest balances. Consolidating debt into a personal loan (if the rate is lower) or utilizing a balance transfer card with a 0% introductory APR could be smart moves, but be mindful of transfer fees and the end of the promotional period.

For those who pay off their credit card balance in full each month, the Fed rate hike will have minimal direct impact. However, for the millions of Americans who carry a revolving balance, the increased cost of debt could become a significant financial burden over the next six months.

Personal Loans: Increased Borrowing Costs

Personal loans, which are typically unsecured and used for a variety of purposes such as debt consolidation, home improvements, or unexpected expenses, will also see their rates rise:

- Higher Interest Rates: Both secured and unsecured personal loan rates will likely increase, making new loans more expensive. Lenders will adjust their rates to reflect the higher cost of capital.

- Impact on Eligibility: While not directly tied to the rate hike, a tightening credit market (which can accompany rate increases) might lead lenders to become more selective, potentially making it slightly harder for some borrowers to qualify for the best rates or even for a loan at all.

- Consideration for Debt Consolidation: For those considering personal loans for debt consolidation, it’s crucial to compare the new personal loan rates against existing debt interest rates (e.g., credit card APRs). If the personal loan rate is still significantly lower, it could be a viable strategy, but the savings might be less pronounced than before the Fed rate hike.

The next six months will be a period where borrowers need to be particularly diligent in comparing offers and understanding the full cost of a personal loan. The days of ultra-low rates are becoming a thing of the past.

Indirect and Broader Economic Impacts

Beyond the direct effects on specific lending products, the Fed rate hike will also have broader implications for the economy and consumer behavior. These indirect impacts, while not always immediately obvious, can significantly shape the financial landscape over the next six months and beyond.

Impact on Savings Accounts and CDs

While borrowing becomes more expensive, saving money might become more rewarding. Banks typically increase the interest rates they offer on savings accounts, money market accounts, and Certificates of Deposit (CDs) in response to a Fed rate hike. This is a positive development for savers, who have endured years of low-yield accounts. Over the next six months, look for higher Annual Percentage Yields (APYs) on these products, making it a good time to consider building up your emergency fund or saving for specific goals.

Business Lending and Investment

Businesses also face higher borrowing costs for expansion, inventory, and operations. This can lead to a slowdown in business investment, which in turn can impact job creation and economic growth. While the Fed aims for a ‘soft landing’ where inflation is controlled without triggering a recession, a significant Fed rate hike always carries the risk of dampening economic activity more than intended.

Consumer Spending Habits

Higher borrowing costs, coupled with persistent inflation, can lead consumers to pull back on discretionary spending. When more of a household’s budget goes towards debt payments and essential goods, there’s less available for non-essential purchases. This shift in consumer spending can have a cascading effect on various industries, from retail to entertainment. Over the next six months, we might observe a more cautious consumer, prioritizing needs over wants.

The Stock Market and Investments

The stock market often reacts negatively to Fed rate hike announcements, as higher rates can increase borrowing costs for companies, reduce future earnings expectations, and make bonds more attractive relative to stocks. While short-term volatility is common, the long-term impact depends on how effectively the Fed manages inflation without stifling economic growth. Investors should review their portfolios and consider how rising rates might affect different asset classes.

Strategies for Consumers: Navigating the New Lending Landscape

Given the anticipated changes over the next six months due to the Fed rate hike, proactive financial planning is more critical than ever. Here are some strategies consumers can employ to mitigate risks and capitalize on potential opportunities.

1. Prioritize High-Interest Debt Repayment

With credit card APRs and other variable-rate loans set to increase, focusing on paying down high-interest debt should be a top priority. Consider the ‘debt snowball’ or ‘debt avalanche’ method to systematically tackle your obligations. The sooner you reduce these balances, the less you’ll pay in interest as rates climb.

2. Evaluate Mortgage Options

- For Prospective Buyers: Understand that your purchasing power might be reduced. Get pre-approved for a mortgage to lock in a rate for a certain period, and factor in higher monthly payments into your budget.

- For Existing Homeowners (with ARMs): Review your adjustable-rate mortgage terms. If your adjustment period is approaching, consult with a financial advisor or mortgage broker to explore refinancing into a fixed-rate loan if it makes financial sense, or prepare for higher payments.

- For Existing Homeowners (fixed-rate): Your monthly payments won’t change, but if you’re considering a Home Equity Line of Credit (HELOC) or a second mortgage, be aware that these rates will likely be higher.

3. Build and Maintain a Strong Credit Score

A good credit score always helps secure better interest rates, but it becomes even more crucial in a rising rate environment. Lenders will be more discerning, and those with excellent credit will have access to the most favorable terms, helping to offset some of the Fed rate hike impact. Pay bills on time, keep credit utilization low, and regularly check your credit report for errors.

4. Boost Your Savings

As interest rates on savings accounts and CDs rise, take advantage of these opportunities to grow your emergency fund and other savings. Shop around for high-yield savings accounts, as different banks (especially online banks) may offer more competitive rates. Having a robust emergency fund is vital in uncertain economic times.

5. Reassess Your Budget

Take a fresh look at your household budget. Identify areas where you can cut back on discretionary spending to free up funds for debt repayment or savings. Understanding where your money goes is the first step towards making informed financial decisions in response to the Fed rate hike.

6. Consult a Financial Advisor

For complex financial situations or investment decisions, a qualified financial advisor can provide personalized guidance. They can help you assess your risk tolerance, adjust your portfolio, and develop a comprehensive plan to navigate the economic changes brought about by the Fed rate hike.

Looking Beyond the Next Six Months: Long-Term Outlook

While our focus has been on the immediate and short-term impacts of the 0.50% Fed rate hike over the next six months, it’s also important to consider the potential long-term outlook. The Federal Reserve’s actions are part of an ongoing strategy to achieve its economic objectives, and further rate adjustments, both up and down, are always a possibility.

The Path of Inflation

The trajectory of future interest rates will largely depend on the path of inflation. If the Fed rate hike successfully cools inflationary pressures, the Fed might slow down the pace of rate increases or even pause them. However, if inflation remains stubbornly high, further significant rate hikes could be on the horizon. Consumers should stay informed about inflation reports and the Fed’s statements to anticipate future monetary policy moves.

Economic Growth and Employment

Another crucial factor is the state of economic growth and the labor market. The Fed aims to bring down inflation without causing a severe economic downturn or a significant rise in unemployment. Monitoring these indicators will provide clues about the Fed’s future decisions. A strong job market might give the Fed more leeway to continue raising rates, while signs of a weakening economy could lead to a more cautious approach.

Adaptability is Key

For consumers, the long-term takeaway is the importance of financial adaptability. The economic environment is dynamic, and interest rates will fluctuate over time. Building good financial habits – like maintaining an emergency fund, managing debt responsibly, and regularly reviewing your financial plan – will serve you well regardless of the Fed’s next move. The recent Fed rate hike is a reminder that financial landscapes are constantly shifting, and those who are prepared are best positioned to succeed.

Conclusion: Preparing for a New Financial Reality

The Federal Reserve’s 0.50% Fed rate hike marks a significant moment for consumer lending and the broader economy. Over the next six months, we can anticipate higher borrowing costs across various credit products, from mortgages and credit cards to personal loans. This adjustment is a direct response to inflationary pressures, and its aim is to stabilize prices, even if it means a period of increased financial scrutiny for consumers.

For prospective borrowers, the era of historically low interest rates is receding, making careful budgeting and credit management more important than ever. Existing borrowers, particularly those with variable-rate loans, must be diligent in monitoring their terms and exploring options to mitigate rising costs. On the flip side, savers may finally see more attractive returns on their deposits, offering a silver lining in an otherwise challenging borrowing environment.

Ultimately, navigating the landscape shaped by this Fed rate hike requires awareness, proactive planning, and a willingness to adapt. By prioritizing debt repayment, re-evaluating financial goals, and seeking expert advice where needed, consumers can position themselves to weather the changes and emerge financially stronger. The next six months will be a test of financial resilience, but with the right strategies, individuals can make informed decisions that safeguard their financial well-being in this evolving economic climate.