Maximize Education Tax Credits 2026: A Family’s Guide to Financial Aid

Anúncios

The dream of higher education for your children is a profound aspiration for many American families. However, the escalating costs associated with college tuition, fees, and related expenses can often feel like an insurmountable hurdle. Fortunately, the U.S. tax code offers several vital provisions designed to alleviate this financial burden: education tax credits. For the 2026 tax year, understanding and strategically utilizing these credits can translate into significant savings, directly impacting your family’s financial well-being and making that dream a more tangible reality.

This comprehensive guide is meticulously crafted to empower US families with the knowledge and actionable steps needed to maximize their education tax credits in 2026. We will delve into the intricacies of the two primary federal education credits – the American Opportunity Tax Credit (AOTC) and the Lifetime Learning Credit (LLC) – along with other crucial tax benefits and planning strategies. Our goal is to demystify complex tax regulations, providing you with a clear roadmap to navigate these opportunities effectively.

Anúncios

Understanding the Landscape of Education Tax Credits 2026

Before diving into the specifics of each credit, it’s essential to grasp the fundamental concept of a tax credit versus a tax deduction. A tax deduction reduces your taxable income, thereby lowering your overall tax liability. A tax credit, on the other hand, directly reduces the amount of tax you owe, dollar for dollar. This distinction is crucial because tax credits often provide a more substantial financial benefit. In the context of education, these credits are designed to offset the costs of tuition, fees, and sometimes even books and supplies for eligible students attending accredited educational institutions.

For the 2026 tax year, the core framework of these credits is expected to remain largely consistent with previous years, though it’s always prudent to keep an eye on any legislative changes that might occur. The key is proactive planning and meticulous record-keeping, as eligibility often hinges on specific criteria related to student enrollment, course load, and adjusted gross income (AGI).

Anúncios

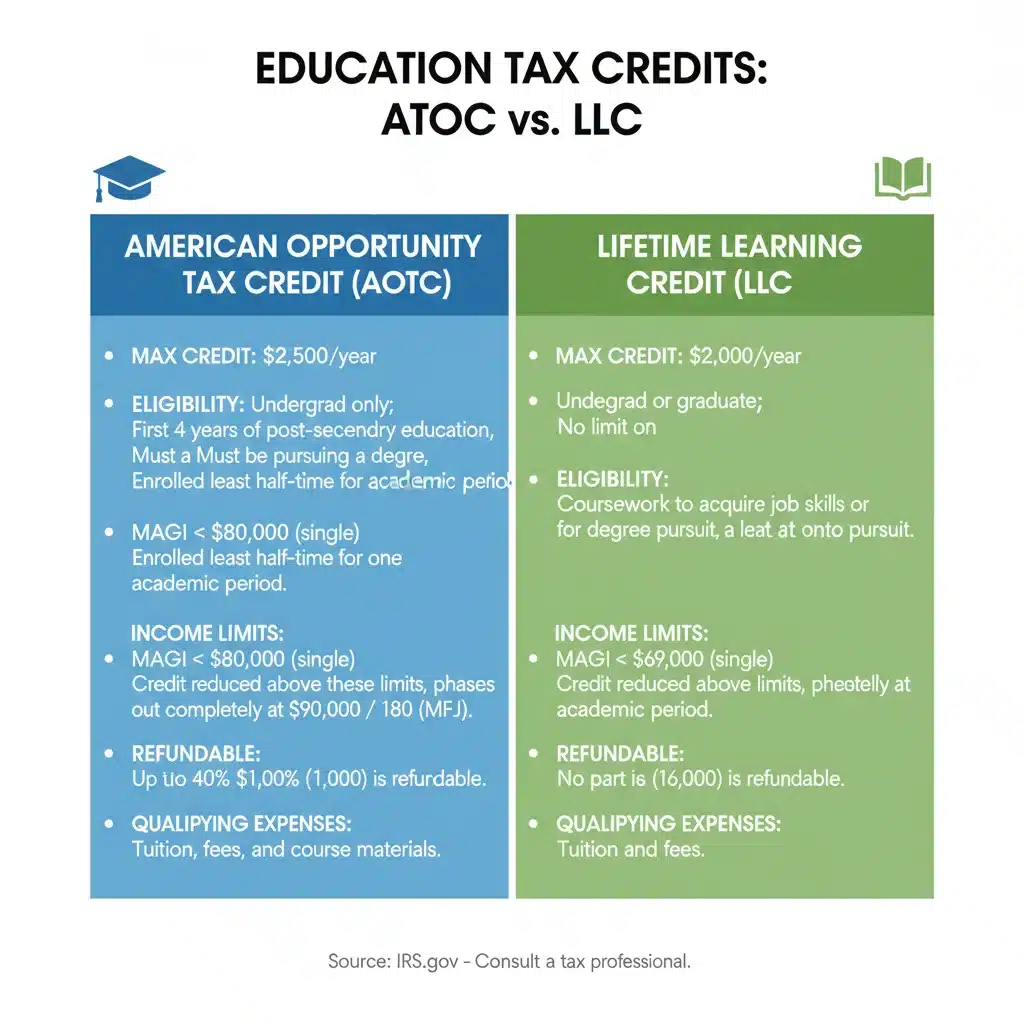

The American Opportunity Tax Credit (AOTC): A Powerful Ally for Early College Years

The AOTC is arguably the most generous of the education tax credits, specifically tailored for students pursuing their first four years of post-secondary education. It offers a maximum annual credit of $2,500 per eligible student. What makes the AOTC particularly appealing is its partial refundability: up to 40% ($1,000) of the credit can be refunded to you, even if it brings your tax liability to zero. This means you could receive money back even if you don’t owe any taxes.

Eligibility Requirements for AOTC:

- Student Enrollment: The student must be pursuing a degree or other recognized educational credential.

- Enrollment Level: They must be enrolled at least half-time for at least one academic period beginning in the tax year.

- Academic Level: The student must not have completed the first four years of higher education (i.e., they are in their first four years of college).

- Prior AOTC Use: The AOTC can only be claimed for a maximum of four tax years per student.

- Felony Conviction: The student must not have a felony drug conviction.

- Qualified Education Expenses: These include tuition, required fees, and expenses for books, supplies, and equipment needed for courses, even if not purchased directly from the educational institution.

Income Limitations for AOTC (2026 Projections – subject to IRS confirmation):

The AOTC is subject to income phase-outs. For 2026, the AGI limits are expected to be:

- Married Filing Jointly: The credit begins to phase out for taxpayers with a modified adjusted gross income (MAGI) between approximately $160,000 and $180,000.

- Single, Head of Household, or Qualifying Widow(er): The credit begins to phase out for taxpayers with a MAGI between approximately $80,000 and $90,000.

It’s crucial to stay updated on the official IRS figures for 2026, as these are subject to change.

The Lifetime Learning Credit (LLC): Flexibility for Continuous Education

The Lifetime Learning Credit is designed for a broader range of educational pursuits, making it ideal for graduate students, those taking a few courses to acquire job skills, or individuals pursuing continuing education. Unlike the AOTC, there’s no limit on the number of years you can claim the LLC, and the student doesn’t need to be pursuing a degree or enrolled at least half-time.

Eligibility Requirements for LLC:

- Student Enrollment: The student must be enrolled in an eligible educational institution for at least one academic period beginning in the tax year.

- Course Purpose: The courses must be part of a post-secondary degree program OR taken to acquire job skills.

- Qualified Education Expenses: These include tuition and required fees. Unlike AOTC, expenses for books, supplies, and equipment are generally not included unless they are required to be paid to the institution as a condition of enrollment.

Credit Amount and Income Limitations for LLC (2026 Projections):

The LLC provides a credit of 20% of the first $10,000 in qualified education expenses, up to a maximum credit of $2,000 per tax return. This is a per-return limit, not a per-student limit, meaning you can only claim a maximum of $2,000 regardless of how many students you have.

- Married Filing Jointly: The credit begins to phase out for taxpayers with a MAGI between approximately $120,000 and $140,000.

- Single, Head of Household, or Qualifying Widow(er): The credit begins to phase out for taxpayers with a MAGI between approximately $60,000 and $70,000.

Again, verify these figures with the IRS for the 2026 tax year. The LLC is non-refundable, meaning it can reduce your tax liability to zero, but you won’t get a refund if the credit exceeds your tax owed.

Choosing Between AOTC and LLC: A Critical Decision

You cannot claim both the AOTC and the LLC for the same student in the same tax year. Therefore, understanding which credit best suits your family’s situation is paramount to maximizing your education tax credits. Here’s a quick comparison to help you decide:

- AOTC is generally more beneficial for:

- Students in their first four years of undergraduate education.

- Families with higher qualified education expenses (up to $4,000 considered).

- Families who might benefit from the refundable portion of the credit.

- LLC is generally more beneficial for:

- Graduate students.

- Students taking a few courses to improve job skills or for personal enrichment.

- Families with lower qualified education expenses (up to $10,000 considered, but only 20% credit).

- Families with students who have already claimed the AOTC for four years.

In many cases, if a student is eligible for the AOTC, it will provide a greater financial benefit due to its higher maximum credit and refundability. However, the LLC provides crucial flexibility for diverse educational paths.

Beyond Credits: Other Education Tax Benefits for 2026

While the AOTC and LLC are the most prominent, several other tax benefits can complement your strategy for maximizing education tax credits. These often come in the form of deductions or tax-advantaged savings plans.

Student Loan Interest Deduction

If you’re paying interest on qualified student loans, you may be able to deduct up to $2,500 of the interest paid each year. This is an above-the-line deduction, meaning it reduces your adjusted gross income (AGI), which can be beneficial for qualifying for other credits and deductions. The deduction is subject to income limitations, which are expected to be around $75,000 for single filers and $155,000 for married filing jointly for 2026, with phase-outs above these thresholds.

Tax-Advantaged Education Savings Plans: 529 Plans and Coverdell ESAs

These plans are not direct tax credits or deductions for the current year, but they offer significant long-term tax advantages for saving for education expenses. Contributions to these accounts are typically made with after-tax dollars, but the earnings grow tax-free, and qualified withdrawals are also tax-free.

- 529 Plans: These are state-sponsored plans that allow you to save for qualified education expenses, including tuition, fees, books, supplies, equipment, and even room and board for students enrolled at least half-time. Many states also offer a state income tax deduction or credit for contributions to their 529 plans.

- Coverdell Education Savings Accounts (ESAs): These are trust or custodial accounts set up to pay for qualified education expenses for a designated beneficiary. Contributions are limited to $2,000 per year per beneficiary, and income limits apply to contributors. Coverdell ESAs offer more flexibility in terms of investment options and can also be used for K-12 education expenses, which 529 plans also now cover.

Using funds from these plans for qualified education expenses does not disqualify you from claiming education tax credits, but you cannot use the same expenses for both a tax-free withdrawal and a credit. For example, if you pay for tuition with a tax-free 529 distribution, you cannot also use that tuition amount to claim the AOTC.

Employer-Provided Educational Assistance

If your employer offers educational assistance, up to $5,250 per year can be excluded from your taxable income. This applies to both undergraduate and graduate courses and can cover tuition, fees, books, supplies, and equipment. This can be a significant benefit for employees looking to further their education without incurring additional tax liability.

Strategic Planning to Maximize Your Education Tax Credits in 2026

Effective tax planning is crucial for optimizing your education tax credits. Here are several strategies to consider for the 2026 tax year:

1. Understand Who Claims the Credit

Generally, either the student or the parent can claim the education credit, but not both for the same expenses. If the student is claimed as a dependent on the parent’s tax return, only the parent can claim the credit. If the student is not a dependent, they can claim the credit themselves. This decision can have significant implications, especially concerning income limitations. Often, if the parents are in a higher income bracket, having the student claim the credit (if they are not a dependent and meet income requirements) might be more advantageous.

2. Coordinate with 529 Plan Distributions

As mentioned, you cannot double-dip. If you take a tax-free distribution from a 529 plan to cover qualified education expenses, you cannot use those same expenses to claim an education tax credit. However, you can strategically use 529 funds for expenses that don’t qualify for credits (like room and board beyond what’s covered by AOTC for books/supplies, or for expenses after the AOTC is exhausted) while using other funds (e.g., out-of-pocket payments) for expenses that do qualify for credits. This intricate coordination can maximize overall tax benefits.

3. Track Qualified Education Expenses Meticulously

The importance of keeping accurate and thorough records cannot be overstated. You’ll need documentation for:

- Form 1098-T from the educational institution (Tuition Statement).

- Receipts for books, supplies, and equipment if not purchased directly from the school (for AOTC).

- Proof of enrollment and academic status.

- Any scholarships, grants, or other tax-free educational assistance received.

The IRS requires these records to substantiate your claims. A well-organized folder or digital system for all education-related financial documents will save you considerable stress during tax season.

4. Consider Income Level and Phase-Outs

The income phase-out ranges are critical. If your modified adjusted gross income (MAGI) is near the upper limits, strategic moves like contributing to a traditional IRA or 401(k) can reduce your AGI, potentially allowing you to qualify for or receive a larger education tax credit. Consult with a tax professional to explore specific AGI reduction strategies.

5. Understand the "Paid Expenses" Rule

For both the AOTC and LLC, the expenses must be paid during the tax year for an academic period beginning in the same tax year or the first three months of the next tax year. For example, if you pay for spring 2027 tuition in December 2026, those expenses can be used for your 2026 tax return. This offers a small window for year-end planning.

Common Pitfalls to Avoid When Claiming Education Tax Credits

Navigating tax law can be complex. Being aware of common mistakes can help ensure you correctly claim your education tax credits and avoid issues with the IRS.

- Claiming the wrong credit: As discussed, AOTC and LLC have different rules. Ensure you meet the eligibility criteria for the credit you choose.

- Double-dipping on expenses: Using the same expenses for both a tax-free 529 withdrawal and an education credit is prohibited.

- Incorrectly reporting scholarships and grants: Tax-free scholarships and grants reduce the amount of qualified education expenses you can use to calculate a credit. Only the amount you paid out-of-pocket (or with taxable financial aid) can be used.

- Missing income limitations: Failing to account for AGI phase-outs can lead to an incorrect credit calculation or even a disallowed credit.

- Inadequate record-keeping: Without proper documentation, the IRS may disallow your claim if audited.

- Not receiving Form 1098-T: Educational institutions are required to send Form 1098-T to eligible students. If you don’t receive it, contact the school. It’s crucial for verifying qualified expenses.

The Role of Form 1098-T in Claiming Education Tax Credits

Form 1098-T, Tuition Statement, is a critical document for claiming education tax credits. Educational institutions send this form to students (and report it to the IRS) by January 31st of the following year. It reports the amount of tuition and fees billed or paid, as well as scholarships or grants received. While Box 1 (Payments Received) is often the most relevant for calculating credits, it’s essential to understand that the amount reported on Form 1098-T might not precisely match your total qualified education expenses. You may have paid for books and supplies not included on the 1098-T, which are still eligible for the AOTC.

Always reconcile the information on your 1098-T with your own records of payments made and expenses incurred. If there are discrepancies, contact the educational institution for clarification or correction.

Future Outlook and Legislative Changes

Tax laws are dynamic, and while the core structure of education tax credits has been stable, minor adjustments or significant reforms can occur. It’s always advisable to consult official IRS publications and, if necessary, a qualified tax professional for the most up-to-date information regarding the 2026 tax year. Subscribing to IRS updates or reputable tax news sources can help you stay informed about any legislative changes that could impact your eligibility or the amount of credit you can claim.

Conclusion: Empowering Your Family’s Educational Journey

For US families, the pursuit of education is a significant investment. By diligently understanding and strategically applying the provisions for education tax credits in 2026, you can significantly mitigate the financial strain of college costs. The American Opportunity Tax Credit and the Lifetime Learning Credit, when combined with other benefits like the student loan interest deduction and tax-advantaged savings plans, form a powerful toolkit for financial planning.

Start early, keep meticulous records, and don’t hesitate to seek professional advice. Empowering yourself with this knowledge not only eases your financial burden but also reinforces your commitment to your family’s educational future. With careful planning, maximizing your education tax credits can help turn the dream of higher education into an affordable and achievable reality for your loved ones.