2026 QCD Changes: Essential Guide for Retiree Charitable Giving

Anúncios

Understanding the 2026 Changes to Qualified Charitable Distributions (QCDs) for Retirees

For many retirees, the desire to give back to their communities and support causes they believe in is a significant part of their financial planning. Qualified Charitable Distributions (QCDs) have long been a powerful tool for achieving this, offering a tax-efficient way to donate directly from an Individual Retirement Account (IRA) to eligible charities. However, the landscape of retirement and tax planning is ever-evolving, and with the passage of the SECURE Act 2.0, significant 2026 QCD changes are on the horizon. These adjustments will have a profound impact on how retirees approach their charitable giving strategies, making it crucial to understand the upcoming modifications.

Anúncios

This comprehensive guide aims to demystify the 2026 QCD changes, providing retirees with the essential knowledge needed to adapt their charitable giving plans effectively. We’ll delve into what QCDs are, how they currently work, and most importantly, what new provisions will come into play in 2026. By understanding these changes, you can ensure your philanthropic efforts continue to be as impactful and tax-efficient as possible.

What Are Qualified Charitable Distributions (QCDs)? A Refresher

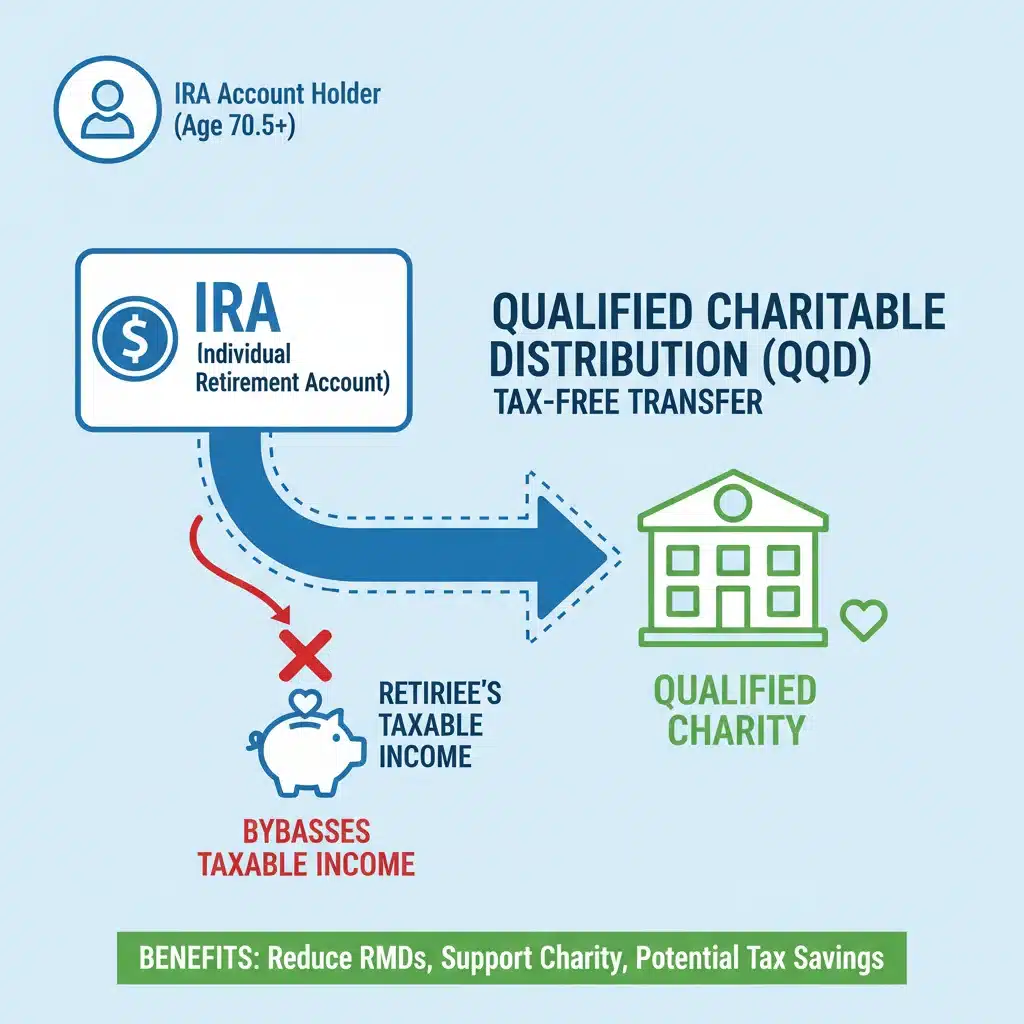

Before we dive into the specifics of the 2026 QCD changes, let’s briefly review the fundamentals of QCDs. A Qualified Charitable Distribution is a direct transfer of funds from an IRA, by the IRA trustee, directly to an eligible charity. This distribution must be made by an individual who is age 70½ or older. The primary benefit of a QCD is that the amount distributed directly to charity counts towards your Required Minimum Distribution (RMD) for the year, but it is not included in your gross income. This is a significant advantage, especially for retirees who might otherwise see their RMDs push them into a higher tax bracket or impact their Medicare premiums.

Anúncios

Key Characteristics of Current QCDs:

- Age Requirement: You must be at least 70½ years old at the time of the distribution.

- Eligible Accounts: QCDs can only be made from traditional IRAs, inherited IRAs, inactive SEP IRAs, and inactive SIMPLE IRAs. They cannot be made from 401(k)s, 403(b)s, or other employer-sponsored plans unless the funds are first rolled into an IRA.

- Eligible Charities: The donation must go to a 501(c)(3) organization. Donor-advised funds, private foundations, and supporting organizations are generally not eligible recipients for QCDs.

- Tax Benefits: The distributed amount is excluded from your taxable income. This is often more beneficial than taking the RMD as income and then claiming a charitable deduction, especially for those who don’t itemize or are subject to deduction limitations.

- RMD Satisfaction: QCDs count towards satisfying your RMD for the year, up to the annual QCD limit.

- Annual Limit: The maximum amount that can be excluded from income as a QCD is currently $100,000 per individual per year.

For years, QCDs have been a cornerstone of tax-efficient charitable giving for retirees, allowing them to support their favorite causes while simultaneously managing their tax liability. However, the legislative landscape is shifting, and the 2026 QCD changes will introduce new dimensions to this established strategy.

The SECURE Act 2.0 and Its Impact on QCDs

The SECURE Act 2.0, signed into law in late 2022, brought about a wide array of changes to retirement planning and savings. While many provisions took effect immediately or in the near future, some, including certain 2026 QCD changes, are set to roll out in the coming years. These delayed effective dates provide a crucial window for retirees and their financial advisors to prepare and adjust their strategies accordingly.

The primary motivations behind these changes are multifaceted. Lawmakers aim to simplify certain aspects of retirement planning, encourage greater charitable giving, and in some cases, adjust the tax implications to better align with evolving economic realities and policy goals. For QCDs specifically, the focus is on providing more flexibility and potentially expanding the scope of their application, albeit with some important new considerations.

Key Provisions Affecting QCDs under SECURE Act 2.0:

- Inflation Adjustment to the Annual Limit: This is one of the most significant 2026 QCD changes. Starting in 2024, the $100,000 annual QCD limit will be indexed for inflation. While this change technically began in 2024, its cumulative effect will be more noticeable by 2026, as the limit will have increased from its original fixed amount. This means retirees will be able to contribute more tax-free dollars from their IRAs to charities over time, keeping pace with economic changes.

- One-Time Election for Charitable Gift Annuities or Charitable Remainder Trusts: This is a brand-new provision, effective in 2023, allowing a one-time election to make a QCD to a charitable gift annuity or a charitable remainder trust. This is a game-changer for individuals who wish to make a substantial charitable gift while also receiving income during their lifetime. However, there are specific limitations and requirements for this one-time election that retirees must understand. This provision, while not strictly a 2026 change, sets a precedent for expanding QCD utility and will continue to be a relevant consideration in 2026 and beyond.

It’s important to note that while the inflation adjustment to the annual limit directly impacts the amount you can give via QCDs, the one-time election for certain planned giving vehicles represents a fundamental shift in the types of charitable strategies that can leverage QCD benefits. Both aspects underscore the evolving nature of charitable giving and tax planning for retirees.

The $100,000 Limit and Its Inflation Adjustment (Starting 2024, Impactful by 2026)

The long-standing annual limit for Qualified Charitable Distributions has been $100,000. This limit has provided a clear ceiling for the amount of tax-free IRA distributions that can be made to charity. However, with the SECURE Act 2.0, this static limit is now dynamic. Beginning in 2024, the $100,000 limit is indexed for inflation. While the immediate impact in 2024 might seem modest, by 2026, the cumulative effect of these adjustments will likely mean a higher annual limit for QCDs, allowing for greater tax-free giving. This is a critical component of the 2026 QCD changes.

For example, if inflation averages 3% per year, the $100,000 limit could be approximately $106,100 by 2026. While this might not seem like a huge jump, for retirees planning significant charitable donations, every extra dollar that can be transferred tax-free is valuable. This adjustment acknowledges the erosion of purchasing power over time and ensures that the real value of the QCD benefit remains consistent for future generations of retirees.

Implications for Retiree Planning:

- Increased Giving Potential: A higher annual limit means retirees can potentially make larger tax-free donations through QCDs, further reducing their taxable income and satisfying a greater portion of their RMDs.

- Strategic Timing: Retirees should consult with their financial advisors to understand the exact indexed limit each year, especially as they approach 2026 and beyond. This will allow for more precise planning of charitable contributions.

- Flexibility in Large Donations: For those considering substantial gifts, the inflation-adjusted limit provides more flexibility to fulfill their philanthropic goals directly from their IRA without incurring additional tax liability.

This subtle yet significant change ensures that the QCD remains a powerful tool for charitable giving, adapting to economic realities and providing ongoing value to retirees. It’s a proactive measure designed to maintain the effectiveness of this beneficial provision well into the future, making the 2026 QCD changes a positive development for many.

The One-Time Election for Life Income Gifts (Effective 2023, Relevant for 2026 Planning)

Perhaps one of the most exciting and complex additions to the QCD landscape, introduced by the SECURE Act 2.0, is the ability to make a one-time QCD election to fund a charitable gift annuity (CGA) or a charitable remainder trust (CRT). While this provision became effective in 2023, its strategic implications will certainly extend into and beyond 2026, making it a crucial aspect of understanding the broader 2026 QCD changes environment.

Previously, QCDs could only be made directly to public charities, providing no income stream back to the donor. This new provision allows retirees to use a QCD to establish a life income gift, offering a unique blend of philanthropy and personal financial security.

Understanding the One-Time Election:

- What it is: A single, irrevocable election to make a QCD of up to $50,000 (indexed for inflation starting 2024) to fund a charitable gift annuity (CGA) or a charitable remainder trust (CRT).

- Key Restrictions:

- It’s a one-time election in a taxpayer’s lifetime. Once made, you cannot make another such election in subsequent years.

- The maximum amount is currently $50,000, indexed for inflation.

- The charitable gift annuity or charitable remainder trust must meet specific requirements to qualify. For CGAs, they must be immediate annuities (payments start within one year) and cannot be deferred. The annuity payments must be 100% taxable as ordinary income.

- The QCD must be made directly from the IRA to the charity that will issue the annuity or manage the trust.

- The donor (and their spouse, if applicable) must be the sole income beneficiaries of the CGA or CRT.

- Benefits:

- Income Stream: Provides a guaranteed income stream for life (CGA) or a set period (CRT) while fulfilling charitable goals.

- Tax-Free Transfer: The initial transfer from the IRA is still excluded from gross income, similar to traditional QCDs.

- RMD Satisfaction: The transfer can count towards your RMD for the year, up to the QCD limit (which for this election is $50,000, indexed).

This new option significantly expands the strategic uses of QCDs. Retirees who might not have considered a direct, outright gift can now explore options that also provide them with a steady income stream, making charitable giving more accessible and appealing. However, the complexity of this provision necessitates careful planning and professional guidance. Understanding the nuances of this one-time election is an integral part of navigating the broader 2026 QCD changes and maximizing your financial and philanthropic impact.

Strategic Planning for the 2026 QCD Changes

With the 2026 QCD changes on the horizon, proactive planning is more important than ever for retirees. These changes offer both opportunities and complexities that require careful consideration. By developing a well-thought-out strategy, you can ensure your charitable giving is both personally fulfilling and financially advantageous.

1. Re-evaluate Your Charitable Giving Goals:

Take this opportunity to review your philanthropic objectives. Do you want to make larger annual gifts? Are you interested in establishing a legacy through a planned gift? The inflation-adjusted annual limit and the one-time election for life income gifts provide new avenues for achieving these goals. Discuss with your family and beneficiaries the impact of your charitable intentions.

2. Understand the Inflation-Adjusted Limit:

Stay informed about the actual QCD limit each year. While the base is $100,000, the indexed amount will gradually increase. Knowing the precise limit for 2026 will allow you to maximize your tax-free contributions. This is particularly relevant for those who consistently contribute close to the maximum amount.

3. Consider the One-Time Election Carefully:

The one-time QCD for charitable gift annuities or charitable remainder trusts is a powerful tool, but it’s not for everyone. Given its irrevocable nature and specific requirements, it demands thorough evaluation. Consider:

- Your Income Needs: Do you need a supplemental income stream in retirement? A CGA or CRT could provide this.

- Your Charitable Intent: Are you comfortable with a portion of your IRA funding a planned gift, knowing the remainder will eventually go to charity?

- Tax Implications: While the initial transfer is tax-free, the income received from a CGA or CRT funded by a QCD will be fully taxable as ordinary income. Factor this into your overall tax planning.

- Professional Advice: This is where the guidance of a qualified financial advisor, estate planner, and tax professional is indispensable. They can help you determine if this option aligns with your comprehensive financial and philanthropic goals.

4. Coordinate with Your RMDs:

QCDs remain an excellent way to satisfy your Required Minimum Distributions without increasing your taxable income. As the QCD limit potentially increases with inflation, you might be able to cover a larger portion of your RMDs with charitable gifts. Ensure your QCDs are properly timed and executed to count towards your RMD for the relevant tax year.

5. Review Your IRA Distribution Strategy:

The 2026 QCD changes might prompt a broader review of your IRA distribution strategy. Are you taking distributions in the most tax-efficient manner? Are there other strategies, like Roth conversions, that could complement your QCD strategy? A holistic approach to your retirement income and giving is crucial.

6. Stay Informed About Further Legislation:

The legislative landscape is dynamic. While the SECURE Act 2.0 has set the stage for the 2026 QCD changes, further legislation could introduce additional modifications. Regularly consult reliable financial news sources and your advisors to stay updated.

Case Studies: Applying the New QCD Rules

To better illustrate the practical implications of the 2026 QCD changes, let’s consider a few hypothetical scenarios:

Case Study 1: Maximizing Annual Tax-Free Giving

- Retiree: Susan, age 75, typically donates $80,000 annually to various charities. Her RMD is $95,000.

- Current Strategy: She uses a QCD for $80,000, satisfying a portion of her RMD and excluding it from income. The remaining $15,000 of her RMD is taken as taxable income.

- Impact of 2026 QCD Changes: Assuming the inflation-adjusted QCD limit reaches $105,000 by 2026. Susan now has the flexibility to increase her QCD to, say, $90,000 or even her full RMD of $95,000 (if her charitable intent matches), all excluded from income. This allows her to fully satisfy her RMD tax-free and potentially increase her charitable impact without incurring additional tax liability.

Case Study 2: Exploring a Life Income Gift

- Retiree: David, age 72, wants to make a significant charitable gift but also needs to supplement his retirement income. He has a substantial IRA balance.

- Current Strategy: David could make traditional QCDs, but these don’t provide an income stream. He might consider funding a CGA with after-tax money, which has different tax implications.

- Impact of 2026 QCD Changes (or rather, the one-time election available since 2023): David could utilize the one-time election to fund a charitable gift annuity with $50,000 (or the inflation-adjusted equivalent) from his IRA. This $50000 is excluded from his taxable income and counts towards his RMD. In return, he receives a fixed annuity payment for life. While the annuity payments are fully taxable, this strategy allows him to make a significant tax-free charitable transfer upfront while securing a guaranteed income stream, addressing both his philanthropic and financial needs. This is a powerful demonstration of the expanded utility of QCDs.

Case Study 3: The Importance of Professional Guidance

- Retiree: Maria, age 78, is aware of the 2026 QCD changes but is unsure how they apply to her complex financial situation, which includes multiple IRAs, a family foundation, and various charitable interests.

- Challenge: Navigating the specific rules for eligible charities (e.g., no QCDs to private foundations), understanding the implications of the one-time election, and coordinating with her overall estate plan.

- Solution: Maria consults with her financial advisor and an estate planning attorney. They help her structure her QCDs to maximize tax benefits, ensure compliance with the new rules, and integrate her charitable giving with her broader legacy planning. They also advise her against using a QCD for her family foundation, as it’s not an eligible recipient.

These case studies highlight that while the 2026 QCD changes offer exciting opportunities, they also underscore the need for personalized advice. Each retiree’s situation is unique, and a tailored approach is essential to harness the full benefits of these evolving provisions.

Potential Pitfalls and How to Avoid Them

While the 2026 QCD changes largely aim to enhance the utility of charitable giving for retirees, there are still potential pitfalls that astute donors should be aware of. Avoiding these common mistakes can save you headaches and ensure your generosity achieves its intended impact and tax benefits.

1. Donating to Ineligible Charities:

QCDs can only go to 501(c)(3) public charities. They cannot be directed to donor-advised funds, private foundations, or supporting organizations. Always verify a charity’s eligibility before initiating a QCD. A distribution to an ineligible charity will be treated as a taxable IRA distribution to you, losing the QCD’s primary tax benefit.

2. Incorrectly Executing the Distribution:

For a QCD to be valid, the funds must be transferred directly from your IRA custodian to the charity. If the check is made out to you first, and then you endorse it to the charity, it will generally be treated as a taxable distribution to you, even if you immediately donate it. Ensure your IRA custodian processes the payment directly to the charity, or that the check is made payable to the charity and delivered by you.

3. Missing the Age Requirement:

You must be 70½ or older at the time the QCD is made. Making a QCD before reaching this age will disqualify it from being treated as such, leading to a taxable distribution. This is a fundamental rule that remains unchanged by the 2026 QCD changes.

4. Exceeding the Annual Limit (or Miscalculating the Inflation-Adjusted Limit):

While the limit is increasing, it’s still a limit. Any amount distributed beyond the annual (inflation-adjusted) QCD limit will be treated as a taxable IRA distribution. Keep track of your total QCDs for the year, and for 2026 and beyond, be sure to use the correct inflation-adjusted figure.

5. Misunderstanding the One-Time Election for Life Income Gifts:

This new provision is complex. Key pitfalls include:

- Not understanding it’s a one-time election: Once you use it, it’s gone for good. Make sure it’s the right choice for your long-term plans.

- Incorrectly structuring the CGA/CRT: The annuity or trust must meet specific requirements (e.g., immediate annuity, 100% taxable income, donor/spouse as sole beneficiaries). Failure to comply will invalidate the QCD treatment.

- Not considering the taxable nature of income: While the initial transfer is tax-free, the income payments from these gifts are fully taxable. This can impact your overall tax picture, especially if you’re relying on these payments for living expenses.

6. Inadequate Record-Keeping:

Always keep meticulous records of your QCDs, including statements from your IRA custodian showing the direct transfer and acknowledgment letters from the charities. These documents are crucial for tax reporting and demonstrating compliance with IRS rules.

By being aware of these potential pitfalls and working closely with your financial and tax advisors, you can confidently navigate the current and upcoming 2026 QCD changes, ensuring your charitable intentions are realized efficiently and effectively.

The Enduring Value of QCDs for Retirees

Despite the complexities and upcoming adjustments, the core value proposition of Qualified Charitable Distributions for retirees remains incredibly strong. QCDs offer a unique intersection of philanthropic opportunity and tax efficiency that few other giving strategies can match. As we move towards 2026 and beyond, understanding and leveraging these provisions will be paramount for savvy retirees.

Why QCDs will continue to be a cornerstone of retiree giving:

- Tax-Efficient RMD Satisfaction: For many retirees, RMDs are a significant source of taxable income. QCDs provide a way to fulfill these obligations without adding to their gross income, potentially lowering their overall tax bill, preserving more of their Social Security benefits from taxation, and even reducing Medicare premiums.

- Reduced Adjusted Gross Income (AGI): By excluding QCDs from gross income, retirees can lower their AGI. A lower AGI can have a ripple effect, potentially qualifying them for other tax credits or deductions, or preventing them from being phased out of certain benefits.

- Enhanced Charitable Impact: By transferring funds tax-free directly from an IRA, more of the donation goes directly to the charity, maximizing the impact of the gift. It removes the ‘middleman’ of personal taxation that would occur if the RMD was taken as income first.

- Flexibility and New Opportunities: The 2026 QCD changes, particularly the inflation adjustment to the annual limit and the one-time election for life income gifts, introduce new levels of flexibility. Retirees can now consider larger annual gifts or integrate their giving with personal income needs in novel ways.

- Simplicity for Non-Itemizers: For retirees who take the standard deduction rather than itemizing, QCDs offer a direct tax benefit that a regular cash donation might not, as the QCD is an exclusion from income rather than a deduction.

The foresight of the SECURE Act 2.0 in adjusting the QCD rules demonstrates a recognition of their importance in retirement planning and charitable giving. While the specifics of the 2026 QCD changes require attention, the fundamental benefit of QCDs as a powerful tool for retirees to support their cherished causes while optimizing their financial well-being remains steadfast.

Conclusion: Preparing for the Future of Charitable Giving

The 2026 QCD changes represent an evolution in the landscape of charitable giving for retirees. From the inflation-adjusted annual limit to the one-time election for life income gifts, these modifications offer both expanded opportunities and increased complexity. For retirees and their families, understanding these changes is not merely an academic exercise; it’s a critical component of effective financial planning and impactful philanthropy.

As you look ahead to 2026 and beyond, consider the following:

- Educate Yourself: Stay informed about the exact inflation adjustments to the QCD limits each year.

- Evaluate Your Goals: Reassess your charitable objectives in light of the new provisions.

- Seek Expert Advice: The intricacies of these changes, especially the one-time election, necessitate consultation with qualified financial advisors, tax professionals, and estate planners. They can help you tailor a strategy that aligns with your unique financial situation and philanthropic vision.

- Plan Proactively: Don’t wait until the last minute. Begin discussions and planning now to ensure a smooth transition and maximize the benefits of the evolving QCD rules.

By embracing these upcoming 2026 QCD changes with a well-informed and strategic approach, retirees can continue to make a profound difference in the world, all while optimizing their personal financial and tax outcomes. Your generosity can be more impactful and tax-efficient than ever before.